Price demand: Price demand refers to various quantities of a commodity that consumers demand per unit of time at different prices, assuming that their incomes, tastes, and preferences and prices of related goods remain constant. The law of demand explains price demand.

Income demand: Income demand refers to the different quantities of a commodity which consumers will buy at different levels of income, other things remaining the same. Other things, here, refer to the price of the commodity, prices of related goods and tastes, and preferences of the consumer. As the income of the consumer increases, his demand for a normal or superior commodity also rises. Thus, there is a positive relationship between income and quantity demanded.

Fig: Quantity demanded for normal or superior good

Fig: Quantity demanded for inferior good

The income demand curve slopes upward from left to right. For inferior goods, the quantity demanded will be more, if the income of the consumer declines, while other determinants of demand remain constant and vice versa. Thus, the income the demand curve slopes downward and it indicates that there is an inverse or a negative relationship between income and quantity demanded.

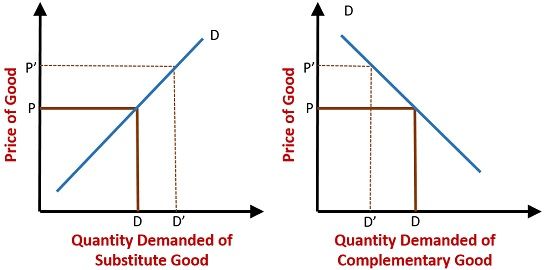

Cross demand: It refers to the different quantities of a commodity that consumers purchase per unit of time at different prices of a related commodity, other things remaining the same. The other things, here, include consumer’s income, tastes and preferences, and the price of the commodity itself. The related commodity may be either substitute or complementary good. For example, tea and coffee are substitutes.

Fig: Demand for substitute goods and Demand for complementary goods

Substitutes satisfy the same want. If the price of tea rises, the consumer buys less of it. Instead, they may buy more of coffee. Thus, a rise in the price of tea increases the demand for coffee. The cross demand curve of coffee in relation to the price of tea will have a positive slope (or, slopes upward to the right). On the contrary, if both the commodities are jointly demanded to satisfy the same want they are called complementary goods. For example, bread and butter are complementary goods. A fall in the price of bread will increase the demand for butter and vice-versa. The cross demand curve of butter in relation to the price of bread will have a negative slope (or slopes downward to the right).

Complementary demand is also known as Joint demand. Joint demand takes place when two or more goods are jointly demanded the satisfaction of a particular want. E.g. bread and butter, shoes and shoe-laces, cup and saucer, tea, milk, and sugar, etc.

Derived demand is another types of demand. The demand for a factor of production that results from the demand for the final form of the commodity which it helps to produce. For example, a consumer buys bread. To bake the bread, bakers have to buy flour. Their derived demand for flour is met by flour mills. The flour mills in turn, buy wheat; their derived demand goes back to the farmers who grow the wheat. The farmers, in turn, have a derived demand for seeds, fertilizers, tractors etc. to cultivate wheat.